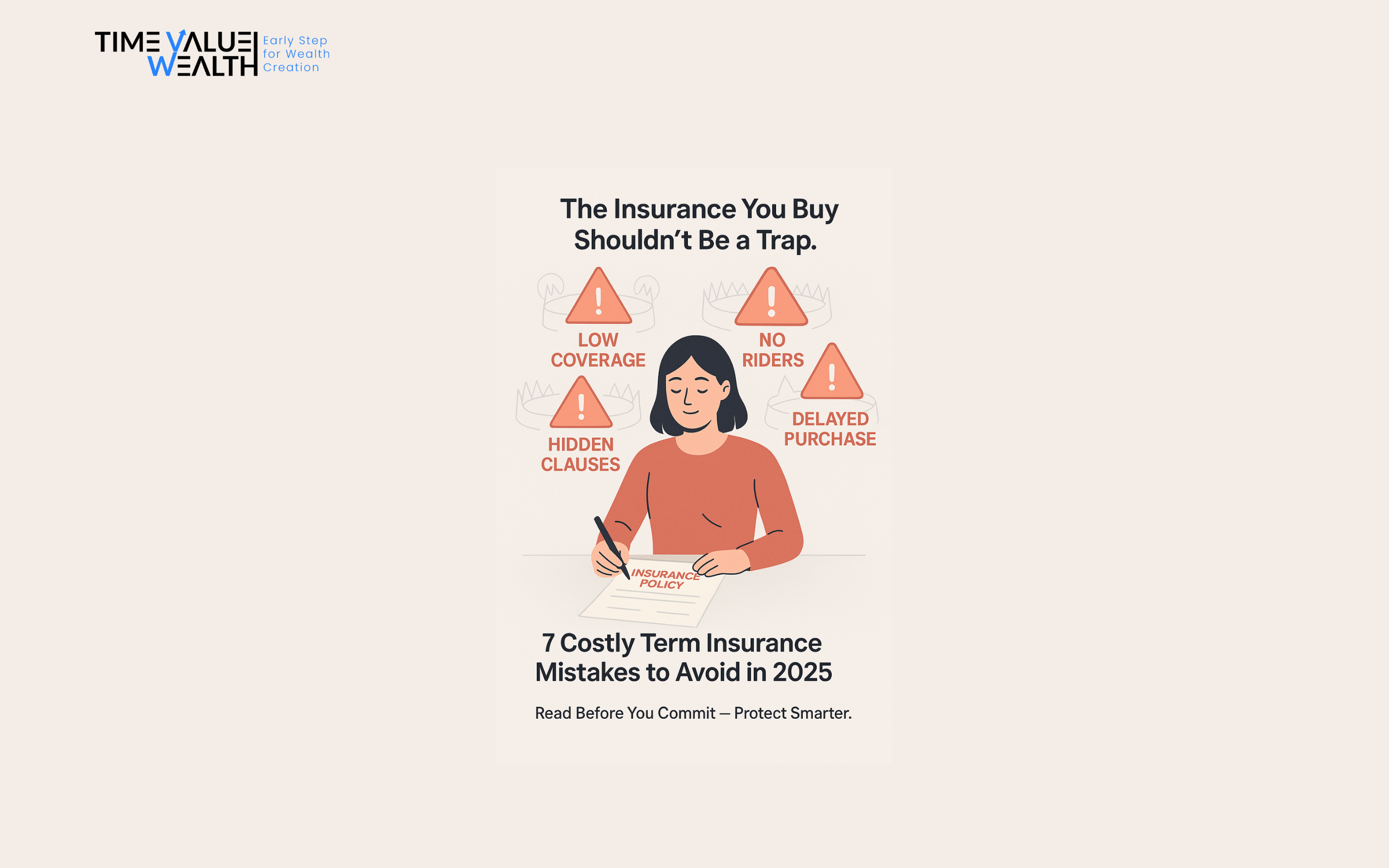

❌ 1. Choosing Low Coverage Just to Save Money

Mistake:

Going for minimal coverage might lower your premium — but it could leave your family financially vulnerable.

✅ Tip: Aim for coverage that’s at least 10–15x your annual income.

❌ 2. Not Disclosing Health Issues or Lifestyle Habits

Mistake:

Hiding medical history or smoking habits can lead to claim rejections.

✅ Tip: Be fully honest in your declaration — it ensures smooth claim processing later.

❌ 3. Choosing the Cheapest Plan Without Research

Mistake:

Lowest-cost plans often have limited benefits, hidden exclusions, or low claim ratios.

✅ Tip: Compare plans based on coverage, riders, and claim settlement ratio — not just price.

❌ 4. Ignoring Riders (Add-ons)

Mistake:

Riders provide extra safety nets — skipping them might limit real-world protection.

✅ Tip: Consider useful riders like:

- Critical illness cover

- Accidental death benefit

- Waiver of premium

❌ 5. Delaying the Purchase

Mistake:

Waiting too long can raise premiums and increase chances of rejection due to health changes.

✅ Tip: Buy in your 20s or early 30s for best rates and smooth approval.

❌ 6. Not Reviewing the Policy Regularly

Mistake:

Life changes — marriage, kids, loans — may require updated coverage, but most forget to revise their plan.

✅ Tip: Review and adjust your plan every 2–3 years.

❌ 7. Relying Only on Employer-Provided Insurance

Mistake:

Company insurance ends with your job. That’s not reliable long-term coverage.

✅ Tip: Always have a personal term plan — it’s your safety net regardless of where you work.

🔑 Final Takeaway

Buying term insurance is smart — but only when done right. Avoiding these mistakes helps protect your loved ones when it matters most.

- Choose sufficient coverage (10–15x income)

- Be transparent with health info

- Use riders for added security

- Update as life evolves

Secure your future smartly — your family’s peace of mind depends on it. 💡